Weekend Roundup

- John Rosier

- Oct 28, 2023

- 2 min read

Magnificent Wells Cathedral

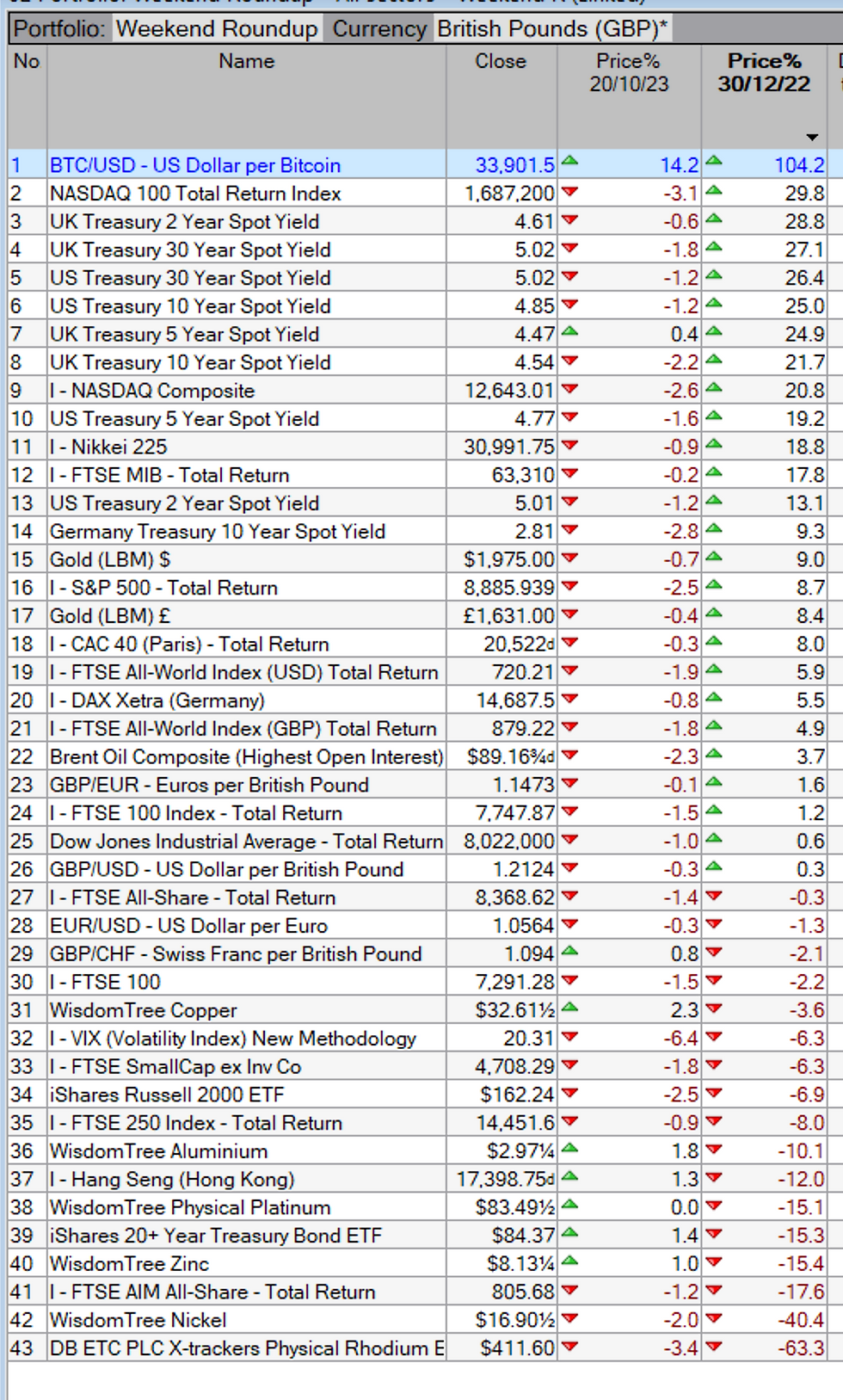

Returns of selected markets over the last week and since 1st January. This week is sorted by the week. Sorted by the last year can be found at the end of this post.

Government bond yields fell over the week. Having hit 5.0%, the US 10-year Treasury yield dropped back as buyers came in and investors such as Bill Ackman publicised that they had closed their short positions. Equity markets also gave up ground, with NASDAQ leading as the “magnificent seven” (Apple, Meta, Microsoft, Nvidia, Amazon, Tesla and Alphabet) started to crack. Meta was down 3.9% and Alphabet -9.9%.

We are now moving into the traditionally more profitable six months from 1st November to 30th April. Let's hope it proves so this time.

JIC Portfolio

The JIC Portfolio had a relatively good week (up 0.3%) and is now down 14.2 per cent in 2023 v -0.3 per cent for the FTSE All-Share (TR) Index.

For the five years to 27th October, it is up 48.7 per cent. Over the same period, the FTSE All-Share TR Index was up 23.7 per cent.

The AIM All-Share is down 17.6 per cent this year, the FTSE 250 is down 8.0 per cent, and the FTSE Small Cap (Ex Investment Co) is down 6.3 per cent.

JIC Funds' Portfolio

The Funds’ Portfolio is down 8.2 per cent this year v +4.9 per cent for the FTSE All-World (GBP, TR) Index.

It is up 17.6 per cent since inception in July 2020. Over the same period, the FTSE All-World GBP TR Index is up 31.0 per cent.

Big Movers over the last week

Positives: IG Design +17.8% and NextEnergy Solar Fund +5.8%.

Negatives: Sylvania Platinum -14.2% (but half of that was it going ex-dividend 5.0p per share), Niox -6.4% and Serica Energy -5.8% (but most of that was due to it going ex-dividend 9.0p per share).

New Three-Month/All-Time Highs last week

VT Argonaut Absolute Return Fund.

New Three-Month Lows

BlackRock Energy & Resources Income, Polar Capital Global Healthcare, Schroder UK Midcap, Strategic Equity Capital, Temple Bar, BlackRock World Mining Trust, Niox, Unilever, Ecora Resources, RS Group, IG Group, Hargreaves Lansdown, Fidelity Asian Values, Global X Copper Miners ETF, and Smithson.

Last week’s trades, news, and ex-dividends

No trades.

Ecora Resources Q3 update was as expected, IG Design results showed good progress on restoring margins, Sylvania Platinum’s Q1 update was below expectations, Bloomsbury Publishing showed solid progress, and Unilever's Q3 results were underwhelming.

BlackRock Energy & Resources Income paid its dividend of 1.1p and Ecora Resources, 1.74p.

Upcoming Events and ex-dividends

Bioventix final results and Glencore production update on Monday.

I’m expecting an update from Harbour Energy and RS Group next week.

Fidelity Asian Values goes ex-dividend 14.5p, Bloomsbury 3.7p and ME Group 2.97p on Thursday.

Brooks Macdonald pays its dividend on Friday.

Cash Holdings

0.8 per cent in the JIC Portfolio and 0.8 per cent in the Funds' Portfolio.

35.3 per cent of the JIC Portfolio comprises six commodity holdings – down from 36.7 per cent last weekend.

Enjoy the weekend.

Comments