Weekend Update: Hoping for the best but preparing for the worst! What next?

- John Rosier

- Mar 28

- 4 min read

Performance Overview

Overall, it was a positive week for my holdings despite a mixed broader market.

My JIC Portfolio was up 2.7% last week, significantly outperforming the FTSE All-Share, which was up 0.36%. Year-to-date (YTD), my JIC Portfolio is up +10.7%, well ahead of the All-Share's +0.4%.

My Funds' Portfolio was up 0.6% last week, while its benchmark, the FTSE All-World (GBP), was down -1.4%. YTD, my Funds' Portfolio is up +4.5%, showing strong resilience compared to the All-World (GBP), which is down -3.2%.

JIC Portfolio Highlights

The JIC Portfolio's strong weekly performance was driven primarily by excellent returns in metals and mining:

Top Performers (1-Week): Fireweed Metals Corp was the standout, surging 18.6%. We also saw double-digit gains from Pollen Street Group PLC (+13.3%) following an excellent year-end update, and Venture Global Inc (+11.1%). Lundin Mining Corp (+8.87%) and Ngex Minerals Ltd (+6.79%) provided solid support.

Laggards (1-Week): The biggest drag was AST SpaceMobile, which pulled back -12.5%. IG Group Holdings (-2.48%) and BH Macro (-2.36%) also saw minor declines.

Funds' Portfolio Highlights

My Funds' Portfolio managed to stay in the green due to its commodity exposure, which successfully offset weakness in global equities:

Top Performers (1-Week): L&G Gold Mining UCITS ETF led the pack, up 6.44%, followed closely by BlackRock World Mining Trust (+4.15%) and CQS Natural Resources Growth & Income (+3.17%).

Laggards (1-Week): Nippon Active Value Fund was the heaviest weight this week, down -5.11%. VanEck Space Innovators ETF (-2.87%) and BH Macro (-2.36%) also closed lower.

Broader Market Observations

Looking at the wider market data, a few key themes drove the week's action:

Commodities Are Running: Brent Oil climbed +2.27% on the week and is now up a staggering 74% YTD. Base metals followed suit, with Aluminium (+2.95%), Copper (+2.09%), and Zinc (+2.02%) all having solid weeks.

Equities Mixed & Tech Heavyweights Struggling: While the FTSE 100 eked out a +0.49% gain, US markets had a tough week. The S&P 500 dropped -2.12%, and the NASDAQ Composite fell -3.23%, dragging down global indices like the FTSE All-World.

Volatility Remains Elevated: The VIX crept up to 27.4 this week, indicating that the broader market remains highly cautious.

What Next?

Macro Outlook: Echoes of the 1970s

Looking at the current macroeconomic landscape, it is hard not to feel a sense of déjà vu. I'm old enough to remember the 1970s—an era defined by the introduction of a national 50 mph speed limit (petrol ration books were printed and issued to motorists in the UK, but they were never actually used), rampant inflation, high taxes, and the gilt market (alongside the IMF), ultimately forcing the government to cut spending.

The "Two Waves" US CPI chart making the rounds right now is what some are calling the most prescient chart crime in history. It overlays inflation from 1966 to 1983 against our current environment from 2013 to today. The trajectory is eerily similar, and the implied path showing current inflation expectations points precisely to the danger of a second, devastating inflationary wave. And remember, as bad as that chart looks for the US, the situation was significantly worse here in the UK.

Geopolitical Risks and Market Realities

While I am hoping for the best—such as the Iranian regime folding—I must position for the worst. My primary fear is that the current geopolitical conflicts drag on with a ground offensive and draw in key regional players like Saudi Arabia and the UAE. Should that happen, we could easily see oil and gas prices spike to $150 a barrel or more.

The implications for economic growth and inflation in that scenario are profound:

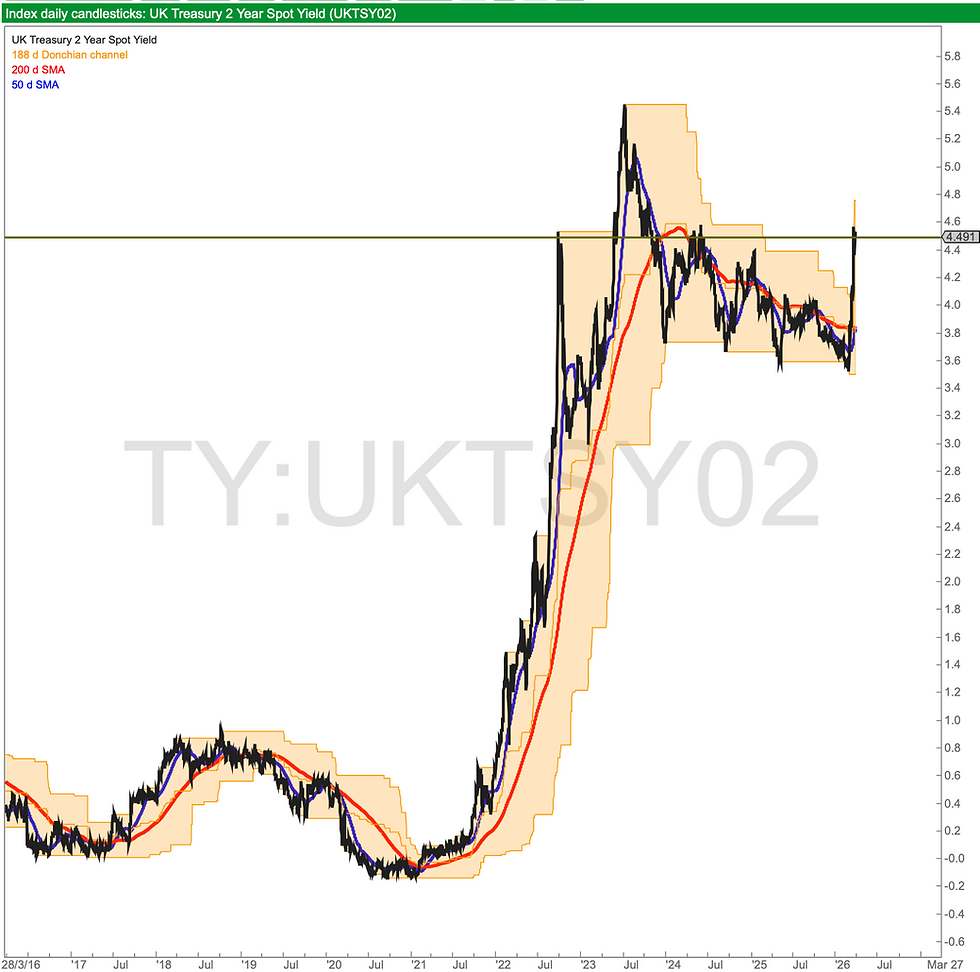

Bonds will offer no protection. The charts I'm tracking for 2-year and 10-year UK gilt yields, as well as the German 10-year yield, are already worrying, showing sharp upward trajectories as the market digests these exact risks.

Equities, particularly high-duration "growth" equities, will struggle heavily under the weight of sustained high rates and input costs.

Gold has seen some recent profit-taking—notably, Turkey reportedly sold 58 tonnes in the two weeks leading up to March 20th—but I'm backing it performing well over the next year, even if the ride is somewhat volatile.

Commodities broadly remain the place to be. They thrive in high-inflation environments, especially when prone to the types of supply disruptions we are starting to see.

Portfolio Positioning

Given this backdrop, I remain heavily exposed to commodities and real assets. I will absolutely not be selling my oil and gas exposure; my positions in Serica Energy, International Petroleum, Venture Global, and the iShares Europe Oil ETF stay intact.

Furthermore, Frontline should continue to perform exceptionally well as shipping day rates spike, particularly given its fleet of 22 Suezmax tankers. In a turbulent, high-inflation environment, BH Macro is also exactly the kind of holding that should prove its worth.

The Balance of Probabilities

While my cash buffer could arguably be higher to pick up bargains if the market legs lower, investing is ultimately about playing the balance of probabilities.

If I am proven to be too pessimistic (and I hope I am), and suddenly, world peace breaks out, the broader market will surge. In that scenario, my portfolios might lag a rapid, broad-based rising market, although I'd expect my Lundin Group companies to still capture a healthy share of the upside.

Regardless of whether we get peace or a prolonged crisis, I am sitting in an enviable position right now: up over 10% in the JIC Portfolio and 4.5% in the Funds' Portfolio so far this year. The strategy is working, and my focus remains on capital preservation and capitalising on structural supply constraints.

Is there a reason why you haven’t included Var Energi in your weekly update John? Or have I missed something?